")

{kind=link}

Your 50,000 PKR in a savings account lost 11,000 PKR last year. Not because you withdrew it, mehangai ate it alive.

Salaried professionals watching petrol climb faster than raises, freelancers paid in dollars but spending in rupees, overseas Pakistanis tired of “qabza mafia” horror stories this is your reality check.

In 2026, SECP is cracking down on scams, SIFC is pumping billions into agriculture/tech, and the filer vs non filer tax gap has widened to 30%.

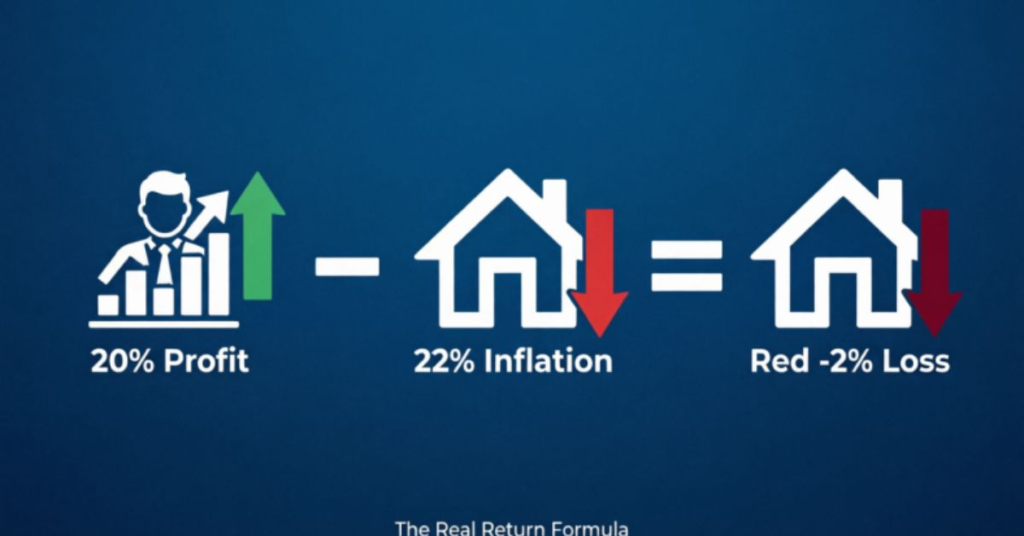

The truth: 20% profit is a LOSS if inflation runs at 22%.

The Real Return Formula

Real Return = (Nominal Return Inflation) Tax

Example: You earned 20% on a mutual fund. Inflation: 22%. Tax: 2% (non-filer). Your real return? 4%. You lost money while thinking you made it.

Quick Summary: Where to Put Your Money in 2026

| Investment Type | Min. Amount | Risk | Expected ROI | Best For |

| REITs | PKR 5,000 | Low to Med | 18 to 25% | Overseas, qabza phobic |

| Mutual Funds (Growth) | PKR 1,000 | Medium | 20 to 30% | Salaried, micro-investors |

| PSX Blue Chips | PKR 10,000 | High | 25 to 40% | Gen-Z, filers only |

| Shariah-compliant Funds | PKR 1,000 | Medium | 18 to 28% | Sood-free investors |

| Gold (Digital) | PKR 5,000 | Low | 12to 18% | Hedge only |

The Filer Advantage: Stop Bleeding 30% in Taxes

Non-filers lose 15 to 30% more in taxes. FBR tightened enforcement in 2026. Banks auto-withhold higher taxes from non filers.

| Investment Type | Filer Tax | Non-filer Tax | Extra Loss |

| PSX Dividends | 15% | 30% | -15% |

| Capital Gains | 12.5% | 25% | -12.5% |

| Bank Profit | 10% | 25% | -15% |

Real Examples:

Stock Dividends: PKR 200,000 earned. Filer: PKR 30,000 tax. Non to filer: PKR 60,000 tax. Lost: PKR 30,000.

Fund Sale: PKR 100,000 profit. Filer: PKR 12,500 tax. Non to filer: PKR 25,000 tax. Lost: PKR 12,500.

Become a Filer (30 Minutes):

- FBR Asaan Tax App or iris.fbr.gov.pk

- Get NTN (24 hours)

- File nil return if under PKR 600,000/year

- Save 15 to 30% for life.

Why Your “Safe” Investments Are Losing Money

National Savings: The -5% Trap

Defense Savings Certificates promise 15% returns. The math:

- Nominal Return: 15%

- Inflation (2026): 20%

- Real Return: -5%

You’re paying the government to hold your depreciating money.

Physical Property: The Qabza Nightmare

“Zameen kabhi ghati nahi” (Land never falls). Tell that to the overseas Pakistani who found someone else’s house on his Bahria Town plot.

Problems in 2026:

- Illiquid (6 to 12 months to sell)

- Qabza mafias in major cities

- Unregulated plot files

- 15 to 20% Capital Gains Tax

- Maintenance eating returns

r/FIREPakistan Reality Check: “Lost 50 lakh in plot file. The developer vanished. No SECP regulation. Don’t be me.” – u/IslamabadInvestor2024

PKR Value Decline vs Investment Growth (2020-2026)

Visual Data: Why Savings Accounts Are Wealth Destroyers

Year | PKR vs USD | Savings (8%) | REITs (20%) | Mutual Funds (25%)

—–|————|————–|————-|——————-

2020 | 168 | 100,000 | 100,000 | 100,000

2021 | 175 | 108,000 | 120,000 | 125,000

2022 | 204 | 116,640 | 144,000 | 156,250

2023 | 278 | 125,971 | 172,800 | 195,312

2024 | 285 | 136,049 | 207,360 | 244,140

2025 | 287 | 146,933 | 248,832 | 305,175

2026 | 280 | 158,687 | 298,598 | 381,469

—–|————|————–|————-|——————-

Real | -40% PKR | +59% nominal | +199% | +281%

Loss | purchasing | = -15% real | = +72% real | = +115% real

Key Insight: While PKR lost 40% purchasing power, REITs delivered +72% real returns and growth mutual funds delivered +115%. Your “safe” savings account actually lost 15% in real terms.

REITs: Real Estate Without the Qabza Mafia

REITs are mutual funds for property. Buy units on PSX, professionals manage buildings/malls, you get rental income + appreciation.

Top REITs:

- Dolmen City REIT: Dolmen Mall. 8 to 10% dividends + 10 to 15% growth. ~PKR 25/unit. Min: PKR 5,000.

- Arif Habib REIT: Offices/warehouses. 7 to 9% dividends. Stable.

How to Buy:

- SECP-licensed broker (Aba Ali Habib, Arif Habib Securities, JS Global)

- CDC account (holds units)

- Buy via app. Commission: 0.1 to 0.3%

- Quarterly dividends

Overseas: Roshan Digital Account. Dividends repatriable.

REITs vs Physical Property

| Factor | Physical (Bahria) | REIT (Dolmen) |

| Entry | PKR 50 lakh+ | PKR 5,000 |

| Liquidity | 6-12 months | 2 minutes |

| Qabza Risk | High | Zero |

| Returns | 10 to 15% | 18 to 25% |

Downsides: Volatility (10 to 15% drops), limited options (2 to 3), not Shariah-compliant.

Verdict: Best for overseas, salaried, qabza-phobic. Physical only for personal use or 1 crore+ in DHA/Bahria 1 to 4.

Regulated Funds: The PKR 1,000 Entry Point

Mutual funds pool your money with thousands of investors. Fund managers buy stocks/bonds on your behalf. All SECP-regulated, held by CDC.

The Daily Dividend Tax Trap

Income/Dividend Funds: Pay monthly/quarterly dividends taxed as income. Non-filers pay 20 to 30% withholding. On 18% returns, you’re left with 12%. Inflation is 20%. You lost 8% real value.

Growth Funds: No dividends. Money compounds inside. Tax only when you sell (12.5% for filers). Defers tax, maximizes compounding.

Best Funds by Category

Conventional Growth:

- JS Growth Fund: 25 to 30% returns. PSX blue chips. Min: PKR 1,000.

- NBP Stock Fund: 22 to 28% returns.

- UBL Retirement Fund: 18 to 24% returns.

Shariah-compliant (Sood-Free):

- Meezan Islamic Fund: 20 to 26% returns. Min: PKR 1,000.

- Al Baraka Islamic Fund: 18 to 24% returns. Shariah Board verified.

- KSE-30 Islamic Index: Lucky Cement, Engro.

Conservative:

- Government Securities Fund: 14 to 16% returns. T Bills/PIBs.

Tip: Start a SIP with PKR 1,000/month. Finja and NayaPay integrate with funds.

PSX (Stock Market): High Risk, Filer-Only Territory

Pakistan Stock Exchange rewards homework, punishes panic. 20 to30% volatility is normal. Filers can see 30 to 40% returns.

2026 Context: PSX hit 95,000+ before correction. Exporters thriving (weak rupee), SIFC money in agriculture/tech.

The SIFC Advantage

Special Investment Facilitation Council pumping billions into:

- Agriculture: Cold storage, seed companies

- IT/Tech: Data centers, software exports

- Energy: Solar/wind to cut imports

Below-market loans, 5 year tax breaks = 30 to 40% margins.

Top Sectors & Stocks

Textile Exporters:

- Weak rupee = 15 to 20% margin boost

- Nishat Mills: 8% dividend, PE 4.5

- Gul Ahmed: 25 to 30% annual returns

Oil & Gas:

- OGDC: 10% dividend, state backed

- PPL: Consistent, low risk

Banking (Not Shariah-compliant):

- HBL, MCB: 8 to 10% quarterly dividends

How to Pick:

- PE under 7 = undervalued

- 5+ years dividend history = reliable

- Debt/Equity under 40% = healthy

Safety Rules

- SECP-licensed brokers: Verify at secp.gov.pk

- CDC holds shares: Safe if broker fails

- Avoid social tips: Already too late

- KSE-100 blue chips: Skip penny stocks

Gold & Overseas Investors: Quick Notes

Gold (12 to 18% Returns): Hedge against inflation, not growth. Digital gold (OneGram, ArifPAK ETF) beats physical (no making charges/storage). Allocate 10 to 15% max.

Roshan Digital Account (RDA): For overseas Pakistanis.

- Buy PSX stocks, REITs, mutual funds directly

- Profits repatriable

- Avoid low yield Naya Pakistan Certificates (11 to 12%) unless you need guaranteed income

Verify Platforms: Avoid Scams

3-Step Verification:

- SECP Registration: Check secp.gov.pk → “Regulated Entities.” Not listed = scam.

- CDC Holdings: All PSX/mutual fund units held by Central Depository Company. Log in to the CDC portal to verify.

- Red Flags: “Guaranteed 40% returns,” unregulated forex/crypto apps, cash-only deals = fraud.

Start Today with PKR 5,000: Your Action Plan

Step 1: Become a Filer (Covered Above) Saves 15 to 30% on taxes for life.

Step 2: Pick Your Entry

Salaried (PKR 5-10K/month):

- Open JS Investments or Meezan account

- Start JS Growth Fund SIP at PKR 1,000/month

- Buy Dolmen REIT with PKR 5,000

- Expected: 22-28% returns

Freelancers (USD/EUR):

- Roshan Digital Account if overseas

- Split: 50% funds, 30% REITs, 20% PSX

- Expected: 25-35% returns

Risk-Averse/Halal:

- 70% Meezan Islamic Fund

- 30% digital gold

- Expected: 18 to 24% returns

Overseas:

- Avoid plot files

- Buy REITs/funds through RDA

- Expected: 18 to 25% returns

Step 3: Automate & Track

- Automate: Standing instruction (PKR 1-5K/month)

- Track Quarterly: Excel (date, value, returns)

- Don’t panic-sell: 10-15% drops normal

- Rebalance Yearly: Maintain allocation

Example: Month 1 to 2: Open, SIP. Month 3: REIT. Result: ~PKR 85K from PKR 70K (20% returns)

The Investment You Don’t Make Is the Real Loss

50,000 PKR in savings earning 8%? You’re losing 12% real value yearly (20% inflation – 8% return). That’s PKR 72,000/year evaporated.

Cousin who bought Nishat Mills in 2023? Up 50%. Friend with Meezan SIP? 28% annual returns. Colleague in cash? Down 20% in purchasing power.

Start small. Start today. PKR 1,000/month compounds to lakhs over a decade.

The best time was 10 years ago. The second best is now.

Conclusion: Your Wealth, Your Choice

In 2026, simply “saving” money is a losing strategy because inflation constantly devalues the Rupee. To protect your future, you must shift from a saver to an investor.

Your Action Plan:

- Become a Filer: It is the single best “investment” to save on taxes.

- Diversify: Don’t put all your eggs in one basket. Spread your money across Mutual Funds, REITs, and a little bit of Gold.

- Start Small, But Start Now: Consistency matters more than the starting amount. Even PKR 2,000 a month can grow into a significant fund over time.

Frequently Asked Questions (FAQs)

1. What is the safest investment option in Pakistan for 2026?

The safest options are Government Securities Funds (T Bills and PIBs). These are backed by the Government of Pakistan, meaning your principal amount is secure, though returns may be slightly lower than the stock market.

2. Can I start investing with only PKR 5,000?

Yes! You can start investing in Mutual Funds and REITs with as little as PKR 1,000 to PKR 5,000. You don’t need millions to begin building your wealth.

3. Why is being a ‘Filer’ so important for investors?

Being a Filer reduces your tax on investment profits by up to 15%. Non-filers face heavy tax penalties that can eat up nearly half of their actual gains.

4. Is digital gold better than buying physical jewelry?

Yes. Digital gold is more efficient because it has no “making charges,” no storage risks, and can be sold instantly via a mobile app at the current market rate.

5. How can Overseas Pakistanis invest without ‘Qabza’ risks?

Overseas Pakistanis should use a Roshan Digital Account (RDA) to invest in REITs and Mutual Funds. These are SECP regulated and digital, meaning no one can “occupy” your investment like physical land.